On 16 November the Reserve Bank of India (RBI) raised risk weights on unsecured loans by banks and non-banking finance companies (NBFCs), and on bank loans to NBFCs. The announcement followed weeks of warnings about the explosive growth in these loans, and marked the first time since 2019 that RBI has used macroprudential tools.

Macroprudential regulation aims to manage risk in the financial system as a whole, rather than in individual institutions. It usually takes the form of changes to risk weights, provisions, exposure limits or loan-to-value ratios. An increase in risk weights results in higher capital requirements for the lender, which is expected to discourage lending and/or push up interest rates.

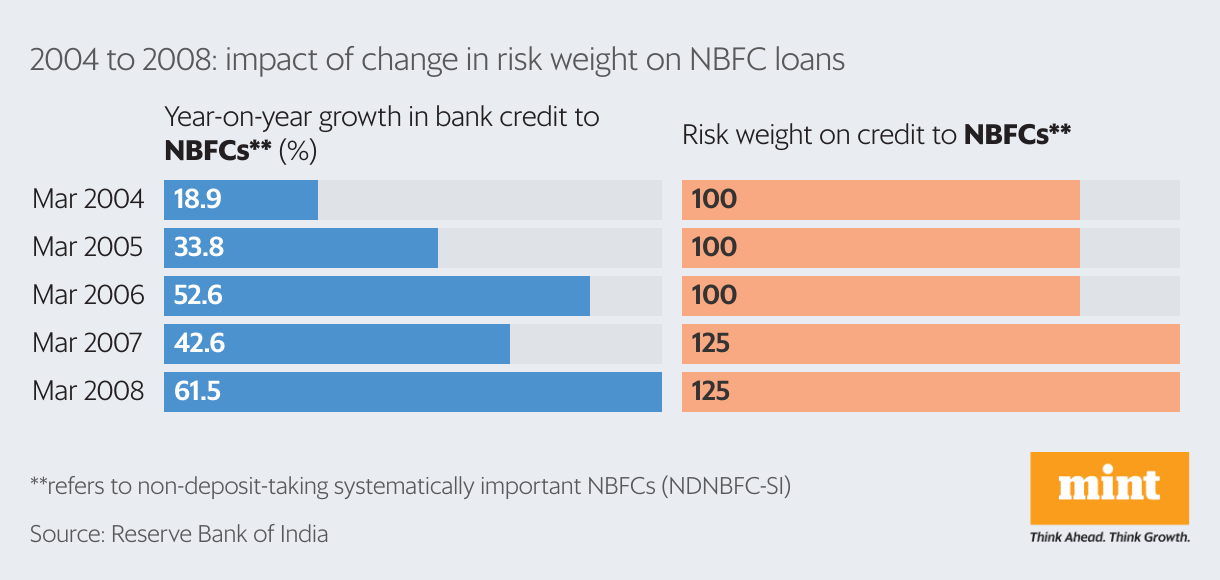

Past experience with such tools has been mixed. During the 2004-2007 credit boom, an increase in risk weights for loans to commercial real estate quickly curtailed credit to that sector, but higher risk weights on loans to NBFCs did not have the same success.

On the other hand, easier credit norms clearly encourage lending. For example, the lowering of risk weights on personal loans (excluding credit card receivables) in September 2019 probably contributed to the rapid growth in consumer credit in the following years.

The timing of the policy — at the fag end of a monetary-tightening cycle — is quite apt. Monetary policy and macroprudential policy work best when aligned, and have reinforced each other in past rate cycles. The RBI’s decision to raise risk weights for specific vulnerable sectors allows it to contain risk without constraining credit to other sectors of the economy.

Household debt

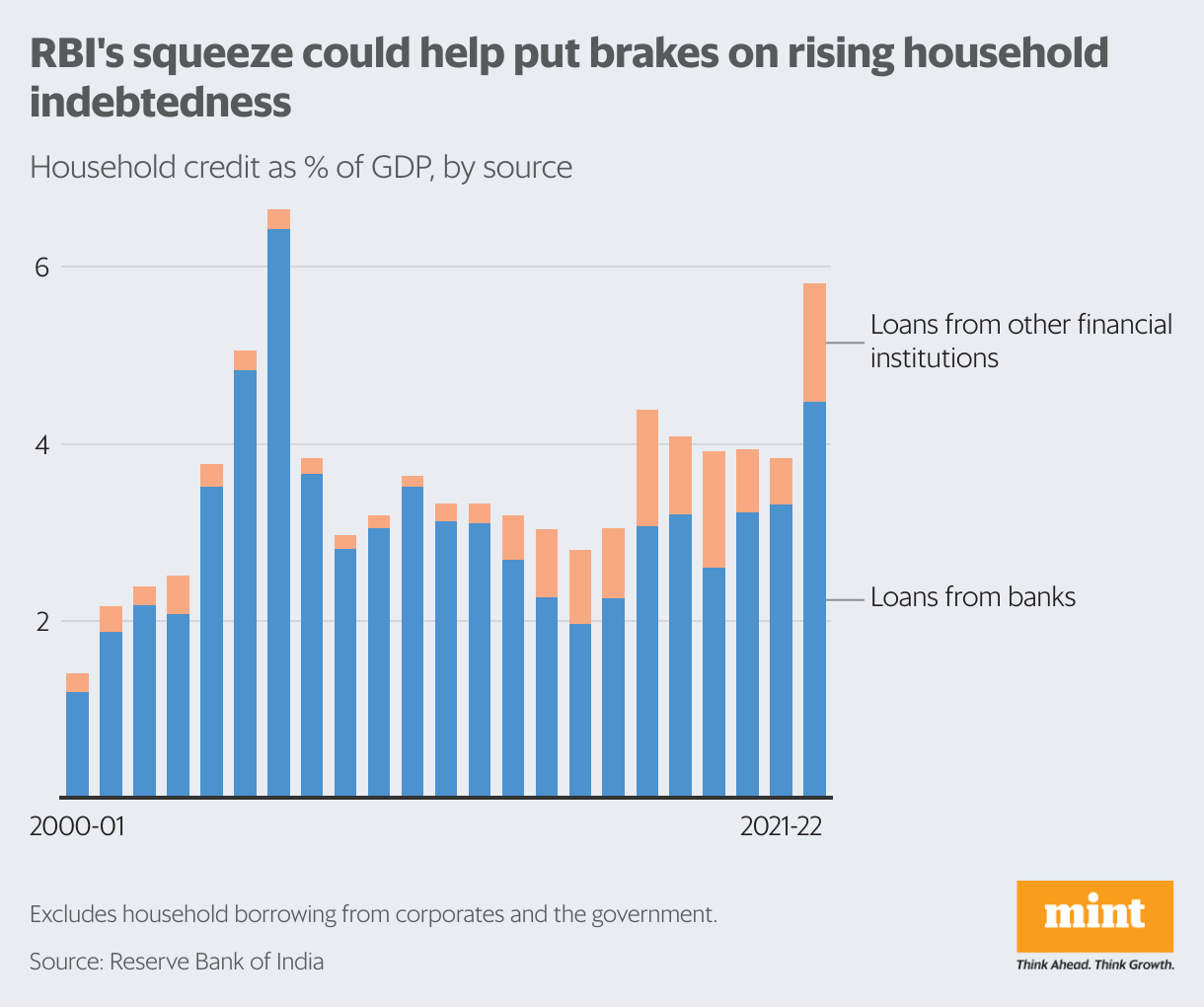

Annual borrowing by households in 2022-23 was 5.8% of GDP, the highest since 2006-07. Not surprisingly, both highs occurred during periods of surging credit, when consumer optimism was high and lenders less cautious. The 2004-2007 boom was followed by corporate loan defaults. This time round there are concerns about the ability of households to service their debt. Between June 2018 and March 2023, outstanding household debt grew rapidly, driven mainly by loans from NBFCs (excluding housing finance and insurance).

Not all this borrowing was unsecured. But the RBI’s warning on the rise in small, unsecured personal loans (below ₹50,000) and reports of rising delinquencies among small borrowers all point to a strain on household finances. Since about 80% of annual household borrowing is from banks and the rest from NBFCs, the RBI action may address the household debt problem to the extent that it limits funding from these sources.

Interconnectedness

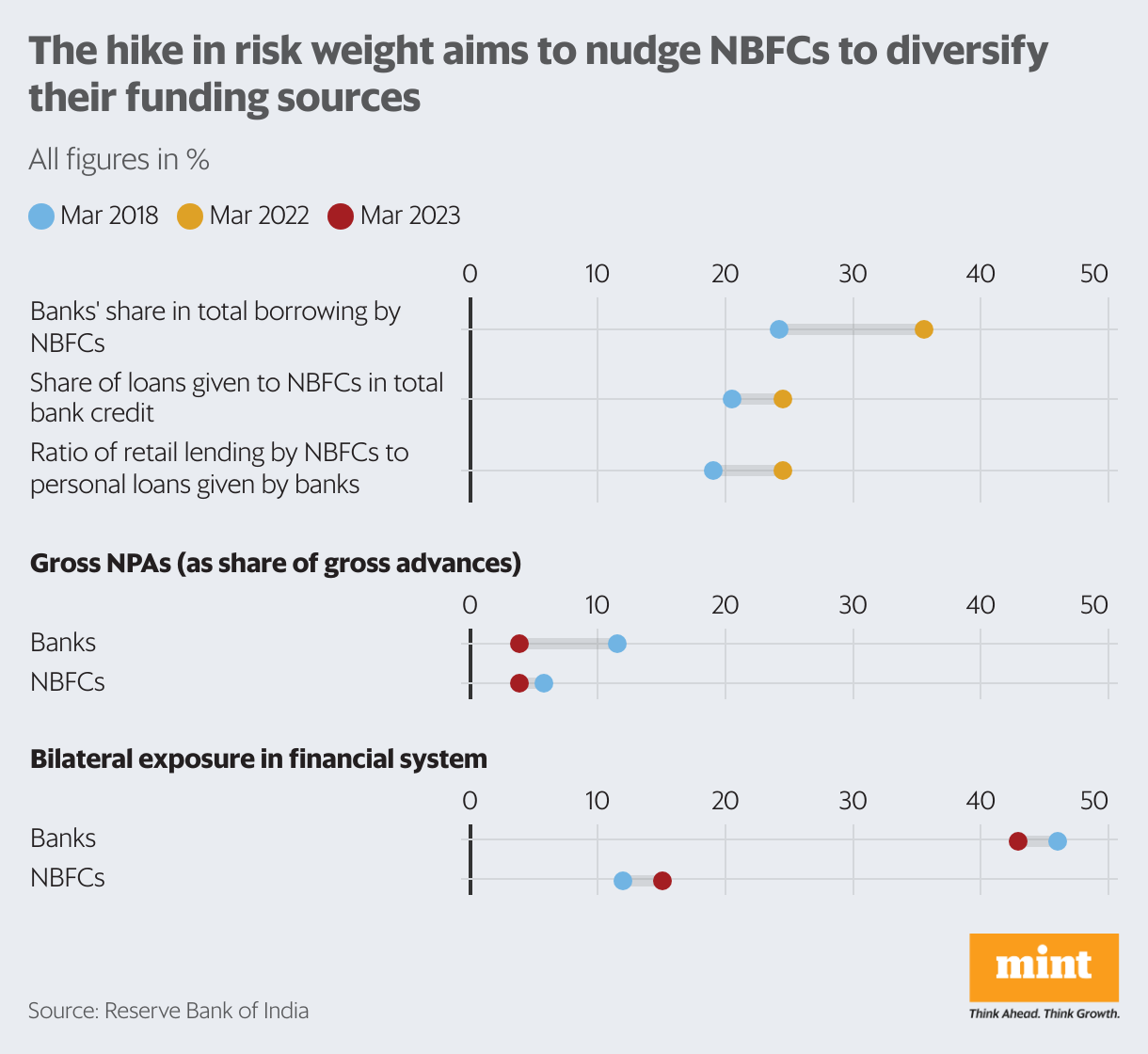

Banks have always been central to our financial system, but the systemic importance of NBFCs has increased in recent years as they have caught up with banks on various metrics. Meanwhile, bank exposure to NBFCs has grown as well. By March 2023, 41.2% of NBFC borrowing was from banks.

RBI research shows that NBFCs are the largest borrowers in the system, followed by private-sector banks. Mutual funds and public-sector banks dominate lending. Each entity is exposed to the other through loans, investments and deposits.

Consider a large private bank that borrows from other banks and mutual funds, and lends to NBFCs, which in turn extend consumer credit. Even relatively small delinquencies in NBFC portfolios would ripple through the entire system.

This risk is shown by the rising share of NBFCs in total bilateral exposures. The recent RBI action aims to change the nature of interconnectedness by nudging NBFCs to diversify their funding sources and strengthen their asset quality.

Capital and risk

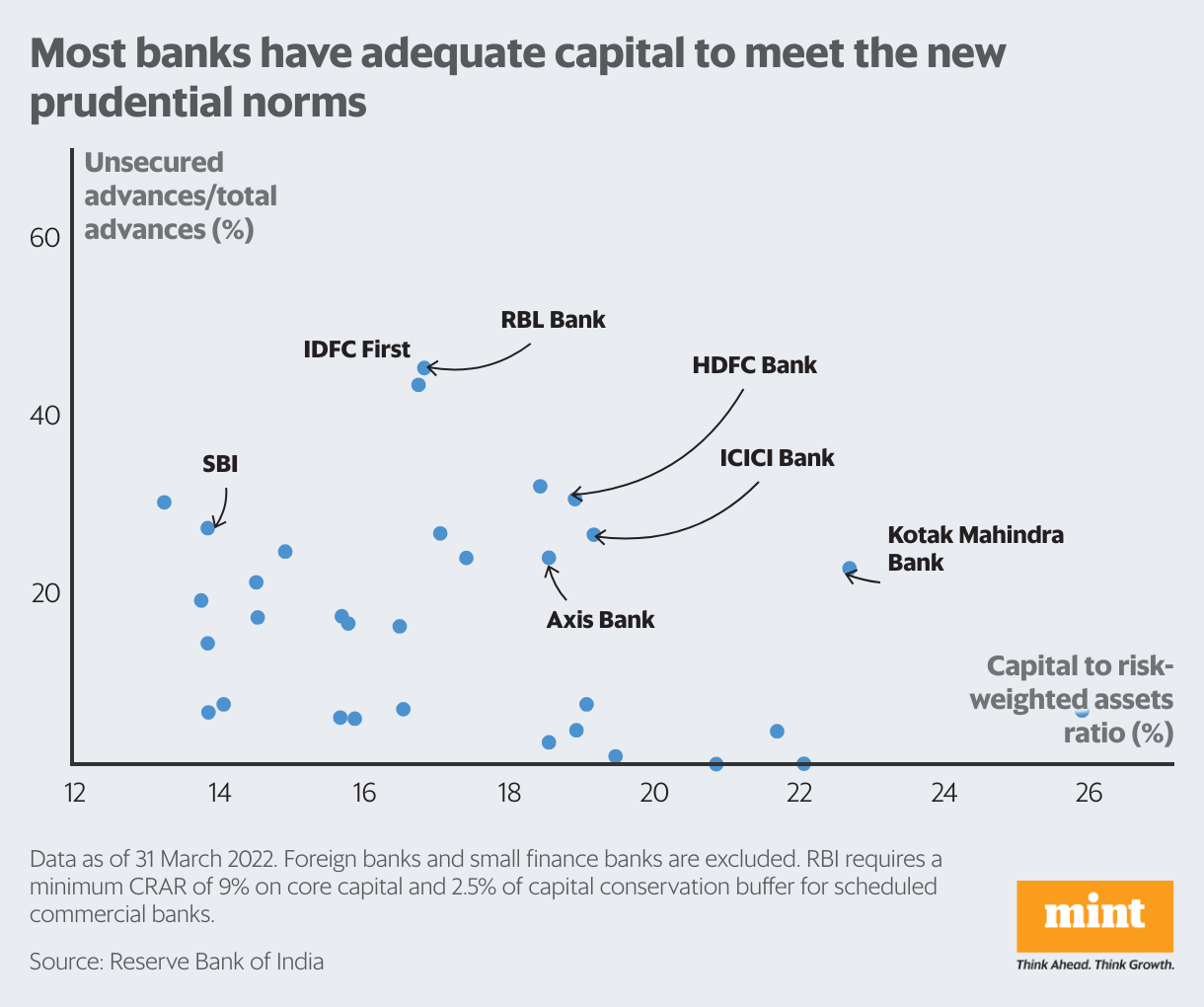

NBFCs, fintech companies and small finance banks are relatively more exposed to unsecured loans, but some large banks have also built up substantial portfolios. However, these banks are not likely to be affected by the new risk weights as they are well-capitalized. There are a few outliers, such as RBL Bank, with a comparatively larger share of unsecured advances and lower capital ratios.

As of the end of March 2022, unsecured loans accounted for more than 20% of total advances in the top five banks. Their proportion has probably increased since then, given the aggressive ramp-up of credit card lending by some private banks.

Even so, adequate capital buffers ensure that none of the large banks are at risk: at worst, their cost of capital may go up slightly. If they end up pulling back a bit on unsecured lending, it will fulfil the RBI’s objective of pruning risk without cutting off credit.

The author is an independent writer in economics and finance.